By Donovan Pyle

Given the economic and human capital challenges businesses face, organizations need to quickly identify opportunities to combat these headwinds by optimizing operating expenses and revamping talent acquisition strategies.

An often-overlooked opportunity typically lies in corporate health plans where small and midsize companies routinely pay for healthcare employees never consumed and companies of all sizes overpay for healthcare employees do consume.

According to a 2019 study, approximately 25% of healthcare spending is wasteful, and with healthcare prices varying widely within any given market, optimizing this area of the business would allow companies to generate interest-free working capital while improving benefits used to attract and retain talent.

An Unsustainable Path:

Before we dive into the tactics needed to achieve optimization, let’s take a look at how destructive traditional health plans — most of which were engineered in the 1990s — have been for businesses and their employee populations.

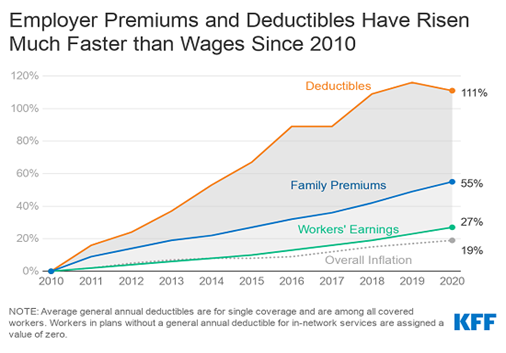

According to one survey, from 2010 to 2021, family premiums rose 55% and deductibles rose 111% faster than wages, and these inflationary pressures are one of the reasons why, in 2010, Starbucks then-CEO Howard Schultz stated that the company spent more money on healthcare than on coffee beans.

If the financial performance of legacy health plans wasn’t bad enough, medical error continues to be one of the leading causes of death in the United States, and commercial health plans receive one of the lowest net promoter scores of any industry.

Given what we know about the unsustainability of legacy insurance products and the opportunity for optimization, it’s not a matter of “if” more employers change the way healthcare is financed and procured, it’s a matter of “when” — and how much financial damage will be incurred in the meantime.

The Healthcare Opportunity:

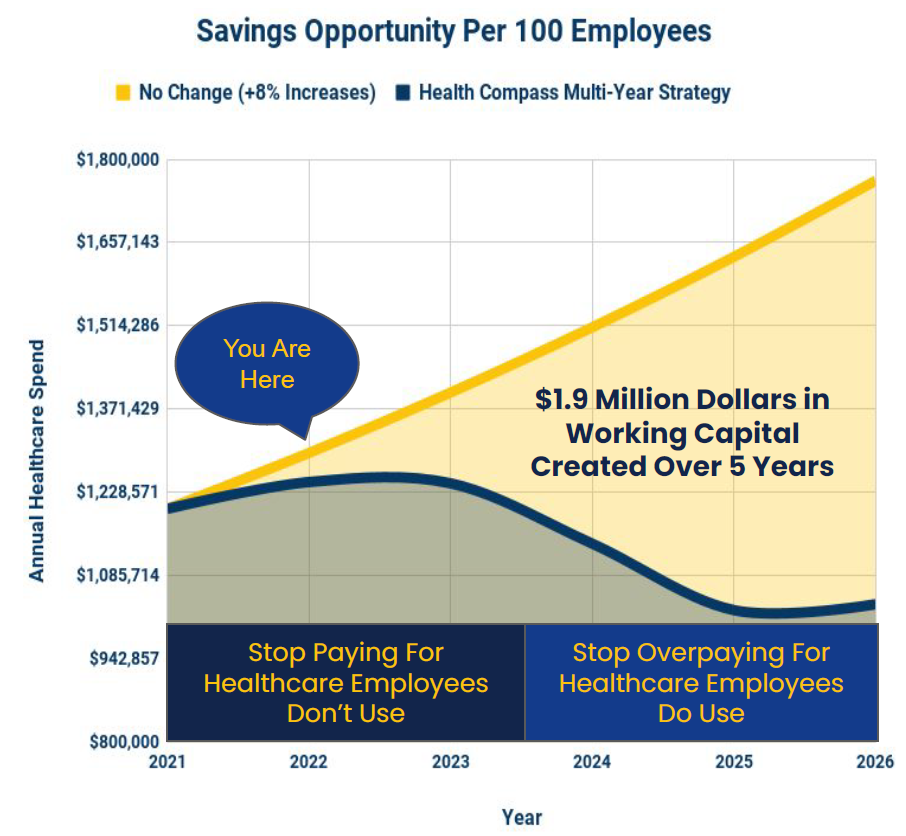

How much interest-free working capital can employers generate by optimizing their healthcare investment? Let’s take a look.

According to some estimates, the average cost of healthcare for each employee is $14,800 a year (paywall), and this number is largely determined by how many spouses and dependents are enrolled, the geography and demography of employee populations and the pricing methodology the health plan uses to pay for healthcare goods and services.

All health plans — regardless of financing and procurement methodologies — consist of fixed costs and variable costs. Fixed costs are made up of things like administrative fees and stop-loss premiums, and typically make up between 20% to 30% of total plan spend for midsize groups. Variable costs are made up of the healthcare goods and services employees and their dependents consume. And as previously mentioned, it’s been well documented that at least 25% of the variable costs are considered waste.

If companies per employee, per year, costs are $14,800, and fixed costs account for 30% of total plan spend, we can assume the savings opportunity is approximately $2,590 per employee, per year. In other words, a company with 1,000 employees enrolled on their health plan has the opportunity to generate $2,590,000 in interest-free working capital each year — without watering-down benefits provided to employees.

Practical Steps For Success:

Every company is at a different point in its healthcare journey, but for small and midsize companies that buy prepaid “fully-insured” plans, here are some first steps.

- Stop paying for healthcare that employees never actually consumed: While businesses like the ease at which prepaid “fully-insured” products are bought, these off-the-shelf products are often financially riskier because your broker has virtually no ability to manage them, and companies inherently end up paying for healthcare that employees never actually consume.

In order to get to the next step in their multi-year strategy, employers need to escape the fully insured marketplace by leveraging one of the many partially self-insured vehicles — that have all the same protections as prepaid products — and ensure businesses only pay for healthcare employees actually consume. - Stop overpaying for the healthcare employees do consume: For employers who have already crossed the partially self-insured threshold, it’s time to improve your healthcare procurement process.

On average, employers unnecessarily pay 241% of what Medicare pays for the same exact services, done at the same exact locations, by the same exact people. Instead of renting legacy carrier networks that use a “discount off of infinity” pricing methodology, employers should consider next-generation networks that achieve price transparency through predictable and stable medicare “plus” methodology that typically, in my experience, results in a net price reduction of 38%.

Since healthcare prices vary greatly within a region, and high-quality care often costs less than low-quality care, employers should reward employees for choosing high-quality/fair-cost care, just like many companies do with travel expenses. This architecture not only saves plans a tremendous amount of money but also eliminates the patient’s out-of-pocket responsibility, which in my experience, often ranges from $1,000 to $5,000.

So as you can see, businesses now have a choice. They can continue to erode profit margins and wages by financing and procuring healthcare the way they always have, or they can strategically and incrementally optimize their health plans to attract and retain talent while generating interest-free working capital that can be leveraged to achieve their goals.